Futures: LME copper was closed overnight. The SHFE copper 2506 contract opened at 77,400 yuan/mt overnight, touched a high of 77,490 yuan/mt at the beginning of the session, then fluctuated downward to a low of 76,640 yuan/mt, and finally closed at 76,760 yuan/mt, up 0.41%, with a trading volume of 45,721 lots and open interest of 164,089 lots.

[SMM Copper Morning Meeting Summary] News: (1) Trump's criticism of Powell has damaged investors' confidence in US assets, causing the US dollar index to plummet to its lowest level since March 2022, finally closing down 0.885% at 98.36. (2) Trump: There is almost no inflation (problem), and he demanded Powell cut interest rates, otherwise economic growth may slow down.

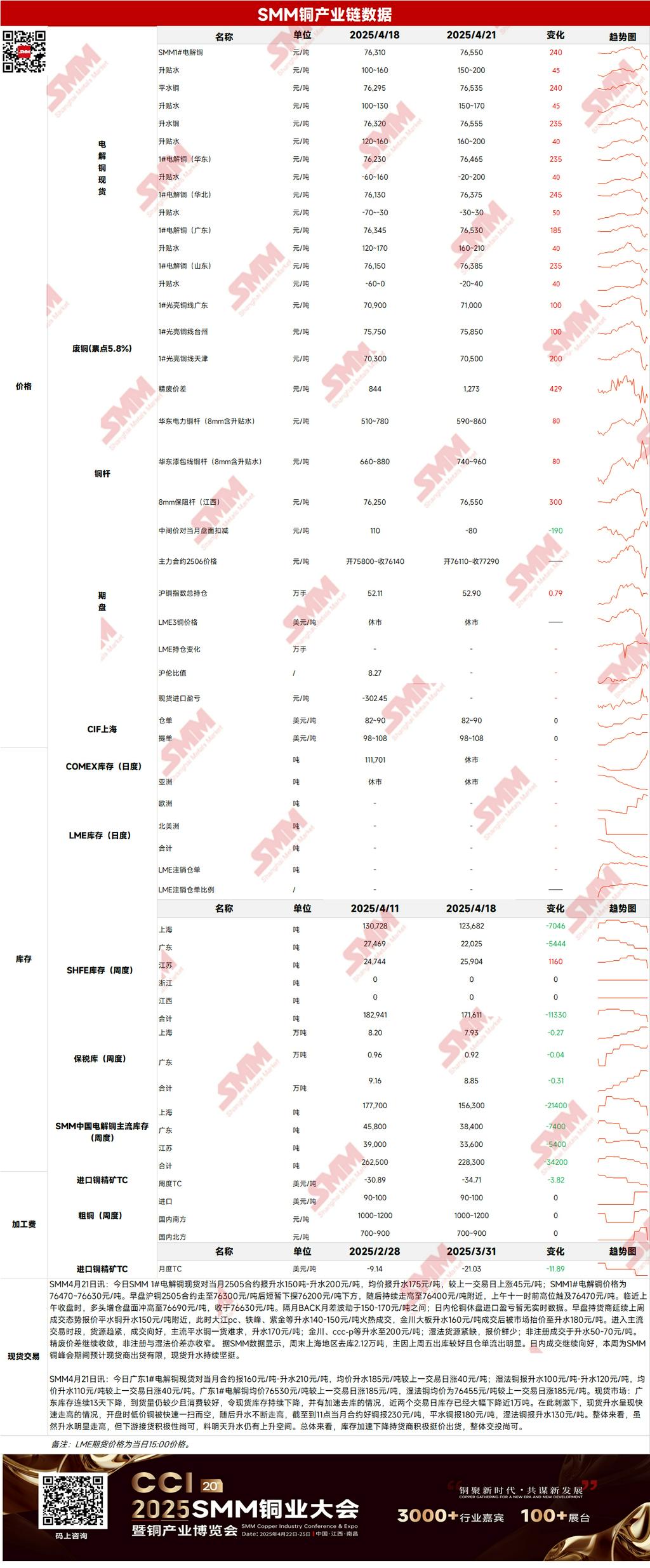

Spot: (1) Shanghai: On April 21, SMM #1 copper cathode spot prices against the front-month 2505 contract were at a premium of 150-200 yuan/mt, with an average premium of 175 yuan/mt, up 45 yuan/mt from the previous trading day. According to SMM data, destocking in Shanghai last weekend was 21,200 mt, mainly due to good outflows from warehouses on Friday and significant warrant outflows. Yesterday's trading continued to improve, and as this week is during the SMM Copper Summit, spot suppliers are expected to have limited shipments, with spot premiums remaining firm.

(2) Guangdong: On April 21, Guangdong #1 copper cathode spot prices against the front-month contract were at a premium of 160-210 yuan/mt, with an average premium of 185 yuan/mt, up 40 yuan/mt from the previous trading day. Overall, with inventories declining rapidly, suppliers stood firm on quotes, and the overall trading was moderate.

(3) Imported copper: On April 21, warrant prices were at $82-90/mt, QP May, with the average price flat from the previous trading day; B/L prices were at $98-108/mt, QP May, with the average price flat from the previous trading day. EQ copper (CIF B/L) was at $55-65/mt, QP May, with the average price flat from the previous trading day, with quotes referring to cargoes arriving in mid to late April. LME copper was closed yesterday, and due to the inability to price, market transactions were scarce. A small number of warrant B/Ls were still offered, with no significant fluctuations in the price center. It was heard that pyrometallurgy B/Ls for late April were offered at $100-105, and three brands for early May were offered at $115-120, QP May. Domestic warrants were offered at around $95/5QP. EQ B/Ls for mid to late May were offered at $60-70/5QP, but transactions were hard to find. Overall, EQ remained firm, but market trading volume decreased significantly. Due to the sharp rise in domestic trade premiums, the SHFE/LME price ratio has room for support, and Yangshan copper premiums are expected to continue to rise next week.

(4) Secondary copper: On April 21, secondary copper raw material prices rose by 100 yuan/mt WoW, with Guangdong bare bright copper prices at 70,800-71,000 yuan/mt, up 100 yuan/mt WoW, and the price difference between copper cathode and copper scrap at 844 yuan/mt, down 142 yuan/mt WoW. The price difference between copper cathode rod and secondary copper rod was 535 yuan/mt. According to the SMM survey, secondary copper import traders said that after stopping purchases from the US, recent supplies from Europe have also decreased, as local production in Europe has decreased and local consumption has increased, leading to suppliers' quotes far exceeding reasonable ranges. It is expected that April purchases will be only 50% of March's.

(5) Inventories: On April 21, LME copper inventories were unchanged; on April 21, SHFE warrant inventories decreased by 12,306 mt to 52,791 mt.

Prices: Macro-wise, sources: The originally scheduled Thailand-US trade talks on April 23 will no longer be held, Vance met with Modi, India is seeking tariff relief from Trump, and India has imposed a 12% tariff on some steel products for 200 days. The US plans to impose new tariffs on solar products imported from Cambodia, Thailand, Malaysia, and Vietnam. Trump said there is almost no inflation (problem) and demanded Powell cut interest rates, otherwise economic growth may slow down. Recently, Trump has repeatedly criticized Powell, reducing investors' confidence in US assets, and the US dollar index plummeted. With the US dollar index falling and increased tariff policies, copper prices closed higher overnight. Fundamentally, with limited domestic arrivals and limited imported copper supplements, coupled with moderate market trading, copper cathode destocking accelerated. As of Monday, April 21, SMM's mainstream copper inventories nationwide decreased by 36,900 mt WoW to 196,500 mt. Compared to last Friday's inventory changes, only Chongqing saw a slight increase, while other regions destocked. Overall, with the US dollar index stopping its decline and running at low levels, copper prices are expected to maintain relatively high levels today.

Click to view the SMM Metal Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]